Happy Friday! South Korean President Yoon Suk-yeol was caught on a hot mic this week labeling U.S. members of Congress “idiots.”

Hey pal, only we get to call them that!

Quick Hits: Today’s Top Stories

-

The U.S. Treasury Department on Thursday imposed sanctions against Iran’s morality police over the recent death of a woman who was in custody for allegedly violating Iran’s dress code. The Treasury Department also sanctioned leaders of Iran’s security forces for the violence perpetrated against those protesting the woman’s death and calling for regime change. According to Hengaw, a human rights watchdog, at least fifteen Iranians have died during the protests, and another 733 have been injured.

-

President Joe Biden announced Thursday that the federal government will foot the entire bill for Puerto Rico’s recovery costs from Hurricane Fiona for the next month, paying for search and rescue, debris removal, power restoration, and other needs. Fiona made landfall on the island Sunday, and, as of yesterday, nearly a million residents remained without power. The storm is expected to reach Atlantic Canada this weekend.

-

Several COVID-19 vaccine mandates have disappeared this week: New York City Mayor Eric Adams announced Tuesday that the city will no longer require vaccines for children participating in after-school activities or mandate that private employers require employee vaccination. Federal Judge Terry Doughty on Wednesday struck down the Biden administration’s vaccine requirement for students and teachers at Head Start, the federal early education program for low-income families. And Canadian Prime Minister Justin Trudeau has reportedly approved letting Canada’s vaccine requirement for border crossings expire on September 30.

-

U.S. District Judge Raymond Dearie—the Mar-a-Lago special master—ordered Donald Trump’s lawyers to state by September 30 whether they think FBI agents lied about documents taken from the Florida resort last month, either by describing them inaccurately or claiming to have retrieved documents that weren’t on the property. Trump has claimed that the FBI planted documents and that he’d declassified the documents marked classified, but his legal team so far hasn’t made those claims in court despite Dearie’s questions.

-

The House on Thursday passed four police funding bills, including the Invest to Protect Act, which would give $60 million a year for five years in grants to local police departments for de-escalation training, body cameras, mental health treatment, recruitment, and other efforts. The legislation faced opposition from the progressive wing of the Democratic Party, and it’s unclear whether or when the bills will pass the Senate.

-

Indiana Judge Kelsey Hanlon issued a preliminary injunction on Thursday temporarily blocking enforcement of the state’s near-total abortion ban. “There is reasonable likelihood that this significant restriction of personal autonomy offends the liberty guarantees of the Indiana Constitution,” Hanlon wrote. The law—which took effect September 15—included exceptions for rape, incest, fatal fetal abnormalities, and to save the life or health of a pregnant woman. Todd Rokita, the state’s attorney general, said he plans to appeal the decision.

-

The Labor Department reported Thursday that initial jobless claims—a proxy for layoffs—rose to a seasonally adjusted 213,000 last week, up 5,000 from the previous week’s revised level of 208,000. The slight increase still leaves jobless claims below the pre-pandemic average of 218,000 in 2019, signaling that the labor market remains tight.

-

The average number of daily confirmed COVID-19 cases in the United States declined about 24 percent over the past two weeks according to the CDC, while the average number of daily deaths attributed to the virus—a lagging indicator—fell 3 percent. About 25,900 people are currently hospitalized with COVID-19 in the U.S., down from approximately 29,700 two weeks ago.

No More Mr. Nice Fed

For a few fleeting weeks there in August and early September, dovish economists—and those blessed with an unmerited sense of optimism—could present a not-totally-crazy case that we’d be able to muddle our way through the inflationary spiral of the last year-and-a-half without sacrificing too much economic growth. Prices, on net, had held steady in July due largely to the falling cost of energy and other commodities. Supply-chain kinks were continuing to unravel. Inflation expectations—among consumers and investors alike—had dropped precipitously as the Federal Reserve continued its belated, but aggressive, campaign of interest-rate hikes.

“A lot of things do point to inflation continuing to come down,” BMO Chief Investment Strategist Yung-Yu Ma told Yahoo Finance in late August. “The most likely scenario is a soft landing.”

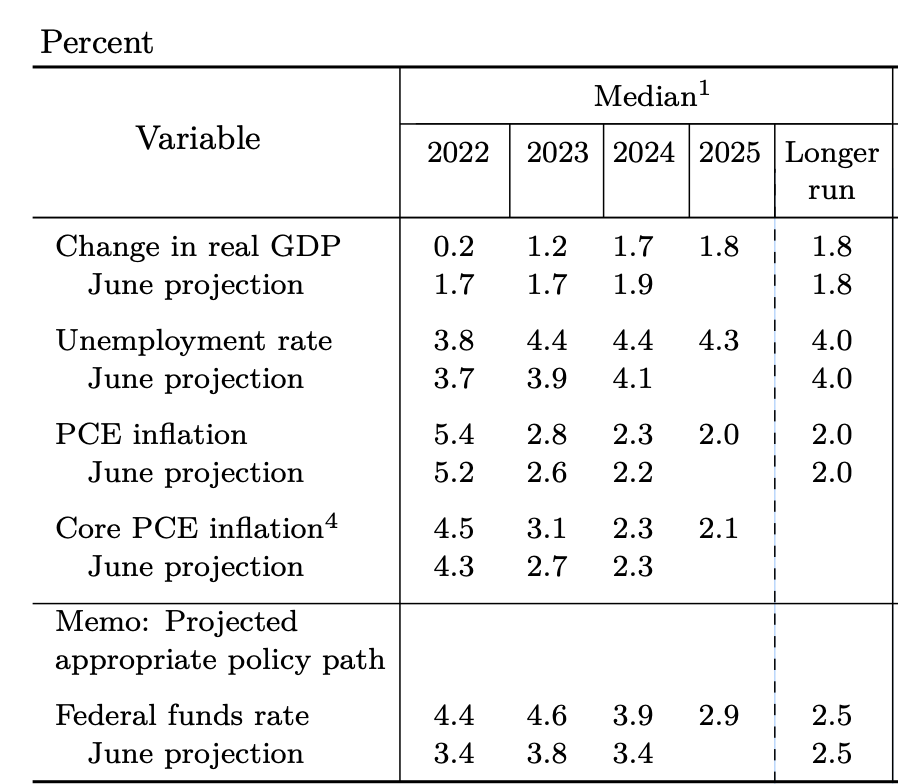

Not anymore. After a disastrous inflation report last week, the Federal Reserve on Wednesday concluded its third consecutive policy meeting with a 75-basis-point interest-rate hike, bringing its target range for the federal funds rate to between 3 and 3.25 percent—the highest level in nearly 15 years. But that figure had been baked into market expectations for weeks; what really startled investors—and sent the Dow Jones Industrial Average tumbling nearly 400 points within minutes of its release—was the Fed’s updated Summary of Economic Projections (SEP) for the rest of the year and beyond.

Everything was a little gloomier than it was just three short months ago. In June, the median Federal Reserve Board member believed the U.S. economy would grow 1.7 percent in 2022, 1.7 percent in 2023, and 1.9 percent in 2024. Now, those expectations are 0.2 percent, 1.2 percent, and 1.7 percent, respectively. The central bankers now forecast unemployment to reach 4.4 percent next year—up from June’s prediction of 3.9 percent—and they extended their timeline for returning annual inflation to their target of 2 percent. Most notably given their role, they now see end-of-year interest rates a full percentage point higher than they did in June—4.4 percent to 3.4 percent—and remaining elevated through at least 2025.

As financial adviser (and frequent Remnant guest) David Bahnsen noted on his podcast earlier this week, Fed projections are “notoriously wrong” and have “one of the worst track records in financial markets.” At this time last year, the central bank expected to end 2022 with interest rates hovering around 0.3 percent—off by a factor of about 15, if these current predictions hold.

But more important than the specific numbers in the SEP is what they signal about the Fed’s intentions. With Wednesday’s report, central bankers made clear they’re not just willing to tip the United States into a recession—they’re almost assuredly going to. “The chances of a soft landing are likely to diminish,” Fed Chair Jerome Powell told reporters this week, referring to a scenario in which prices stabilize without a dramatic rise in unemployment. “We have got to get inflation behind us. I wish there were a painless way to do that. There isn’t.”

Central banks around the world are arriving at the same conclusion. The Bank of England boosted target interest rates by 50 basis points on Thursday to the highest level the United Kingdom has seen since 2008, and rates in Switzerland are positive for the first time in nearly a decade after its national bank hiked them yesterday by 75 basis points. South Africa and Canada have both announced 0.75-percentage-point hikes of their own this month, while Norway opted for a smaller but still-aberrant 0.5 percentage points. Sweden’s central bank experimented earlier this week with its largest rate increase in decades, and Japan intervened in the foreign exchange market for the first time since 1998 in an effort to strengthen the yen.

These countries’ moves were all made primarily in response to their own inflation woes, but many central banks also see utility in keeping pace with the Fed to stabilize their currencies. “Higher U.S. rates have bolstered the dollar, exacerbating inflation elsewhere by raising the cost of commodities which are, more often than not, priced in the greenback,” Claire Jones notes in the Financial Times. “The consequences of the Fed’s mistakes are effectively exported from the U.S., burdening America’s trade partners.”

Powell & Co. are aware of this phenomenon—but don’t expect them to change course for the sake of overleveraged economies around the globe. “We regularly discuss what we’re seeing in terms of our own economy and international spillovers, and it’s a very ongoing, constant kind of a process,” Powell said. “[But] of course we all serve a domestic mandate, domestic objectives—in our case the dual mandate, maximum employment, price stability.”

Looking only at the consumer price index (CPI) report for August that was released last week, it’s difficult to find evidence that the Fed’s crusade thus far has made any progress toward the second half of that dual mandate. Topline annual inflation fell for the second straight month—to 8.3 percent—but that was due almost entirely to falling gas prices, a trend with multiple contributing factors that cannot be expected to continue. The cost of food grew at a 9.6 percent annual pace in August, and—excluding both energy and food, which are generally seen as more volatile than other sectors—core inflation actually picked up.

“This is a much much worse CPI report than anyone was expecting,” Justin Wolfers—professor of public policy and economics at the University of Michigan—said at the time. “The decrease in headline inflation due to lower energy prices is there, but the underlying rate—best proxied by core inflation—is running a fair bit higher than anyone forecast and most of us hoped.”

Interest rate hikes are a blunt tool, and their effects often lag months behind their implementation—particularly with economic indicators like CPI. But as Megan McArdle points out in her latest column, there are some signs the Fed’s new posture is beginning to cool the economy—if you know where to look.

30-year fixed-rate mortgages in the United States have more than doubled over the past year, and now sit above 6 percent for the first time since 2008. Sales of previously owned homes declined for the seventh straight month in August, down 19.9 percent year-over-year. And asking rent prices just fell month-over-month for the first time since December 2020.

Worth Your Time

-

The New York Times offers a glimpse—based on analysis of 160,000 files from the Kremlin’s internet regulator—into the digital crackdown underway in Russia. “Four days into the war in Ukraine, Russia’s expansive surveillance and censorship apparatus was already hard at work,” Paul Mozur, Adam Satariano, Aaron Krolik, and Aliza Aufrichtig write. “Roughly 800 miles east of Moscow, authorities in the Republic of Bashkortostan, one of Russia’s 85 regions, were busy tabulating the mood of comments in social media messages. They marked down YouTube posts that they said criticized the Russian government. They noted the reaction to a local protest. Then they compiled their findings. One report about the ‘destabilization of Russian society’ pointed to an editorial from a news site deemed ‘oppositional’ to the government that said President Vladimir V. Putin was pursuing his own self-interest by invading Ukraine. A dossier elsewhere on file detailed who owned the site and where they lived.”

-

New data suggests New York’s bail reform increased re-arrest rates—and likely overall crime. “Perhaps the increase in crime identified above will be offset by a reduction in future offending, given the long-run criminogenic effects of jail,” Charles Fain Lehman writes in a piece for the Manhattan Institute’s City Journal. “On the other hand, the most relevant study to New York finds that the incapacitating effect of jail pretrial slightly outweighs its criminogenic effect post-release, at least within the study period. In any case, those effects are heterogenous. Some detainees are career criminals, for whom the benefits of keeping them behind bars almost certainly outweigh criminogenic costs; others are not. One thing is clear: bail reform did not make it easier for judges to distinguish between criminals. Instead, it shifted the balance of detention against public safety—and, as John Jay College of Criminal Justice’s Michael Rempel noted during a public discussion of the data on Wednesday, it did so without closing the much-discussed racial gap in detention that it was largely intended to do.”

-

It’s been a while since we all learned to pronounce another Greek letter. Carl Zimmer’s latest article explains why the Omicron label has survived multiple new subvariants—and provides a look at what’s coming down the pike. “10 months have passed since Omicron’s debut, and the next letter in line, Pi, has yet to arrive,” he writes. “That does not mean SARS-CoV-2, the coronavirus that causes Covid-19, has stopped evolving. But it may have entered a new stage. Last year, more than a dozen ordinary viruses independently transformed into major new public health threats. But now, all of the virus’s most significant variations are descending from a single lineage: Omicron. ‘Based on what’s being detected at the moment, it’s looking like future SARS-CoV-2 will evolve from Omicron,’ said David Robertson, a virologist at the University of Glasgow. It’s also looking like Omicron has a remarkable capacity for more evolution. One of the newest subvariants, called BA.2.75.2, can evade immune responses better than all earlier forms of Omicron. For now, BA.2.75.2 is extremely rare, making up just .05 percent of the coronaviruses that have been sequenced worldwide in the past three months. But that was once true of other Omicron subvariants that later came to dominate the world. If BA.2.75.2 becomes widespread this winter, it may blunt the effectiveness of the newly authorized boosters from Moderna and Pfizer.”

Something Cool

We didn’t know exactly what to expect last night at our first-ever regional event, but the turnout at Party Fowl in Franklin, Tennessee, blew us away. As our community manager Ryan likes to say at the end of every staff meeting: “The state of our community is strong.”

A huge thank you to everyone who came out—we can’t wait for the next one! Stay tuned for more details in the coming weeks. And keep an eye out for announcements of some terrific new speakers coming to “What’s Next?”, our post-election conference in Naples, Florida. More information here.

Presented Without Comment

Also Presented Without Comment

Also Also Presented Without Comment

Toeing the Company Line

-

Equal parts petulant and ominous? Sounds like a typical speech by Russian President Vladimir Putin, Klon writes in the latest edition of The Current (🔒). But just because the leader’s Wednesday remarks hit familiar themes doesn’t mean we should ignore them, Klon argues, suggesting a U.S. response that’s calm, measured, unflinching, and cognizant of the fact that this war may have a long way yet to go.

-

About that speech… Sarah, David, Steve, and Jonah all discuss Russia’s mobilization and the implications of Putin’s nuclear chest-thumping on the latest episode of the Dispatch Podcast. They also tackle the state of politics around immigration (spoiler: still a mess) and offer some rank punditry about Democrats’ recent surge in polling.

-

Thursday’s Stirewaltisms (🔒) comes to us from Arizona, where Chris is examining the state’s latest angry chapter in its decade of miserable politics. “With just a little more than six weeks to go before the 2022 midterms,” he writes, “Arizonans are being afflicted with a truly dreadful cycle that has been a lot about the 2020 election and too little about the future of one of the fastest-growing and increasingly prosperous states in the union.”

-

On the site today, Audrey and Harvest take a look at Democratic Rep. Tim Ryan’s attempts to style himself a moderate as he campaigns for Ohio’s open Senate seat. Kevin Williamson writes about the grift of telling people what they want to hear, and, in today’s Boiling Frogs, Nick Catoggio argues that Putin’s mobilization strategy in Ukraine is likely to collapse—but that doesn’t mean he can’t still inflict a lot of pain on the rest of the world.

Let Us Know

As of 9:03 p.m. ET last night, it’s officially autumn. What’s your favorite thing about the greatest season of the year?

Please note that we at The Dispatch hold ourselves, our work, and our commenters to a higher standard than other places on the internet. We welcome comments that foster genuine debate or discussion—including comments critical of us or our work—but responses that include ad hominem attacks on fellow Dispatch members or are intended to stoke fear and anger may be moderated.

With your membership, you only have the ability to comment on The Morning Dispatch articles. Consider upgrading to join the conversation everywhere.