Dear Capitolisters,

Believe it or not, this is Capitolism’s two-year anniversary, and I can’t think of a better topic to cover for the big celebration. Anyway, on to the show:

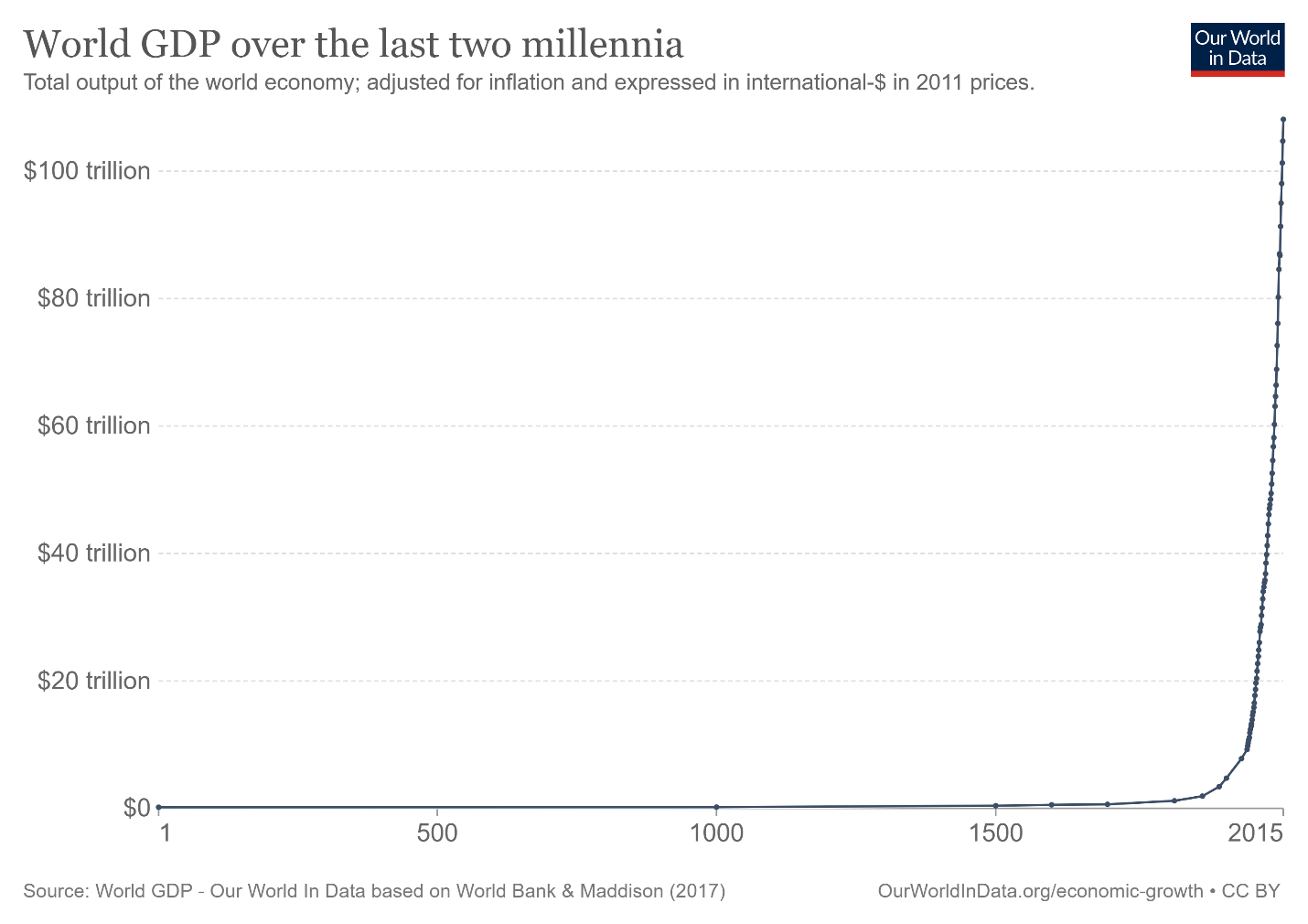

As you all know, I’m a fan of charts. (Yes, okay, that’s an understatement; let’s move on.) If done right, they convey immense amounts of information in just a glance, quickly settling debates on important issues. Yet one of my favorite charts—and one that I think explains so much about so many topics—is often ignored in our policy and political discourse:

As the chart shows, and as Jonah and others have discussed at length, humans suffered through millennia of misery, with little change in wealth or living standards, and then something miraculous happened around the 18th century: Economic growth exploded. And, even after wars and famines and everything else, it never really looked back. It’s a pretty incredible visual—one mirrored at the country and individual levels (though more staggered over time). And you’d think it’d be something policymakers are constantly noting and probing for answers to today’s big challenges. What happened? Why did it happen? And how can we keep it going? (Etc.)

Yet, when you bring up the radical improvement in global and per capita gross domestic product over the last few centuries, the reaction is rarely that kind of optimistic curiosity. Instead, it’s skepticism, if not outright derision. These data fail to consider, so the argument goes, widespread environmental destruction, rampant inequality, persistent global poverty, or the ever-increasing burdens on the working class.

(It is, quite frankly, exhausting.)

Fortunately, a new book from Gale Pooley and my Cato colleague Marian Tupy (hereafter P&T), Superabundance, thoroughly dismantles those claims, effectively ending the famous debate between economist Julian Simon and biologist author Paul Ehrlich about population growth and resource availability that we first discussed back in April. Bolstering their previous research with mounds of new data and plenty of beautiful charts, P&T show that the “hockey stick” graph above indeed warrants praise and consideration: Across all sorts of metrics and for basically everyone on the planet, things are indeed getting better (almost) all the time—not despite population growth, but because of it.

Yet as I read the book over Labor Day weekend (as one does), I surprisingly found myself struck less by the charts (which are still great; don’t get me wrong) and more by the authors’ clear explanation of why things are so much better today than they were a century, or even a few decades, ago.

In short, it’s all about free exchange—something every policymaker should realize, especially today.

But First, the Data

Before we get to that, however, let’s first establish that we are, contra all the pessimists and doomsayers, living in a relatively miraculous age. To show that, P&T walk readers through their methodology, data, and findings, which focus on (but are certainly not limited to) “time prices” (TPs)—essentially the amount of time your average worker must work to afford a wide range of goods and services, calculated by dividing an item’s nominal money price (no inflation adjustments) by a worker’s nominal hourly income. We’ve discussed this concept a bit in previous columns, but it warrants elaboration given its centrality to the book’s thesis.

So let’s take a simple example: TVs. According to P&T’s calculations, an unskilled worker and a blue-collar worker in the 1997 United States made $7.49/hour and $18.12/hour, respectively, while a 42-inch LCD TV that year cost a whopping $15,000 (again, these are all nominal, unadjusted figures). Thus, the TV’s time price in 1997 was ridiculously high: an unskilled worker would have to work about a year (2003 hours) to afford that TV, while a blue-collar worker would have to work a mere (ha) 828 hours. That’s not just a luxury for almost all Americans, but a total fantasy.

P&T convincingly argue that these time prices are a preferable way to assess the availability of resources over time and across countries for several reasons:

First, innovation (or productivity gains) shows up in many places, including lower prices and higher incomes. To capture the full impact of innovation, therefore, we must look at changes in both money prices and incomes. To look at just money prices only tells half the story. TPs make it easier to see the whole picture. Second, TPs transcend all of the complications associated with subjective and disputed inflation adjustments such as the Consumer Price Index (CPI), the Implicit Price Deflator (IPD), and the Personal Consumption Expenditures price index (PCE). TPs use the nominal price and nominal income at each point in time. No inflation adjustments are necessary. Third, analysts can use a variety of hourly income rates (e.g., hourly wage, hourly compensation that includes non-wage benefits, etc.) to calculate the TP. Fourth, TPs can be calculated using any currency and any point in time. Fifth, income and prices are converted to time, which is objective and universal.

I can tell you today that the LCD TV was $15,000 in 1997, but that number’s meaningless unless you also know what the average person was earning back then. And using nominal hourly compensation avoids various calculation and comparison issues—there are no inflation or other adjustments, and an hour is an hour is an hour always and everywhere.

Having established TPs as their preferred metric, P&T then set about tracking TPs for tons of goods over various time periods, some stretching back to the 1850s. Returning to our TV example, you’ll not be shocked to learn that a flatscreen TV’s time price has collapsed: By 2019, the unskilled/blue collar worker made more—$13.66 and $32.36, respectively—and the TVs cost much, much less ($148). Thus, P&T show that an item that no one could afford in the 1990s requires just a few hours of work today. (And the TV’s also a lot better, but we can leave that alone for now.)

To help readers further understand changes in personal abundance between two dates, P&T provide additional calculations, such as (1) the Personal Resource Abundance Multiplier (pRAM), which is the number of items that a worker can buy for the same amount of labor over the time period; (2) the percentage change in Personal Resource Abundance (pRA), which measures the pRAM’s rate of change over that same period; (3) the compound annual growth rate of Personal Resource Abundance (CAGR-pRA), which calculates the speed at which the item has become cheaper each year; and (4) the doubling period (YD-pRA), which shows the time required for a specific item to become twice as affordable. These are shown in the table below for TVs:

Thus, for the same amount of time that a blue collar worker had to work to afford one LCD TV in 1997, he could today buy 181 TVs (pRAM)—a 18,000 percent improvement in personal resource abundance over the whole period (PRA).

TVs are, of course, an extreme (but easily-understandable) example of declining time prices. Superabundance thus examines literally hundreds of other items, ranging from basic commodities to food, finished goods, and certain services (which they acknowledge are more difficult to measure). P&T also provide several in-depth examples of declining TPs and increasing personal abundance over time—sugar, breakfast, Thanksgiving dinner (which we discussed last year), pickup trucks, air travel, computation, housing, air conditioning, etc. In almost every case, they find that time prices declined over the period examined for the average American and his counterparts abroad—and often substantially (though they can and did occasionally increase from year-to-year). There are dozens of charts demonstrating all of this—along with detailed data and hundreds of calculations to show the authors’ work. I can’t/won’t show you them all (buy the book!), but here are two more.

First, we see a total collapse in U.S. time prices for retail goods since the the 1970s:

Second, to show how free(ish) markets can boost even less-tradable services, P&T show a decline in time prices (and thus an increase in personal abundance) of lightly regulated cosmetic procedures in the United States:

Pretty cool stuff. And there’s plenty more in the book.

These findings alone would be sufficient for a book-length refutation of the pervasive economic pessimism in the U.S. and elsewhere, but P&T go further by examining how our increasing abundance correlates with population growth. To do this, they examine whether various goods and services have become more or less abundant—as measured in time prices (“pRAM,” above)—as global population has increased. They find that, for all 18 datasets examined, personal abundance increased at a faster pace than population growth. They deem this “Superabundance” and provide a great data visualization tool to show how it works:

Using finished goods again as an example (see Figure 5.21 above), we see here that the average U.S. worker in 2019 could buy a lot more stuff for his hour of labor than he could back in 1979 (Y axis), even as population expanded (X axis)—resulting in “superabundance” for the U.S. population as a whole (red box expands to green box).

This can all be difficult to conceptualize, I admit. Fortunately, P&T provide a simple example of how to think about it all: a pizza party. The Personal Resource Abundance (pRA) measures the size of a slice of pizza per partygoer, and Population Resource Abundance (PRA) measures the size of the entire pizza that you’re serving. When you invite more people to the party, there can be three basic outcomes:

-

Misery. If population increased while pRA declined, this would be like inviting more people to the party but keeping the entire pizza the same size: the slices (pRA) have to get smaller to feed the crew. As we saw in the first hockey-stick chart, this Malthusian/Ehrlichean worldview—one of finite resources, perpetual scarcity, and legitimate fears about overpopulation—described much of human existence.

-

Stasis. If pRA remains the same as population increases, the pizza pie grows in line with your guest list, thus allowing everyone to enjoy a same-sized slice, regardless of the number of attendees. That’s surely better than the first party, but it’s not really progress.

-

Superabundance. With Superabundance, however, something truly magical happens: pRA grows at a rate that’s faster than population growth. In other words, our pizza pie is growing faster than the party’s guest list; thus, every new partygoer means we each get an even bigger slice of ‘za. Yum.

In all 18 cases, pRA increased at a faster pace than the population grew. In other words, the size of the slice of pizza per person increased at a greater rate than the rate of new party attendees. Going back to the real world, economist and author George Gilder summarizes the topline conclusions in the book’s preface:

Going back to 1850, the data collected by Tupy and Pooley show that for more than a century and a half, measured by time prices, resource abundance has been rising at a rate of 4 percent a year. That means that every 50 years, the real-world economy has grown some sevenfold. Between 1980 and 2020, while population grew 75 percent, time prices of the 50 key commodities that sustain life dropped 75 percent. That means that for every increment of population growth, global resources have grown by a factor of 8. Tupy and Pooley confirm [Julian] Simon’s revolutionary insight: people are not a burden on resources but the source of them.

Surely, resources aren’t everything in life (though they’re still essential for it), and P&T supplement their abundance analysis with plenty of other data on long-term improvements in things like health, environmental quality, political freedom and social tolerance, and so on. But the point of their resource analysis isn’t that we should celebrate humans’ modern ability to consume 181 TVs (or whatever); it’s that we should celebrate humans’ relatively sudden and incredible ability to generate more essential resources in less time, even as more people inhabit the planet, thus increasing not only our consumption but also our ability to pursue happiness beyond it. This, not the TVs stuff, is why time prices are so important:

Time is essential because it is the scarcest commodity of all. Everyone, rich and poor alike, dies in the end. The more time we spend at work, the less time we have for other pursuits such as leisure or time spent with our loved ones. Or, as Adam Smith put it, “The real price of everything is the toil and trouble of acquiring it. … What is bought with money … is purchased by labour.”

Though our lives today surely feature real challenges, we can work less to have much more—an incredibly optimistic reality that far more people should be cheering.

So, What Explains Superabundance?

Pooley and Tupy next turn to explain what has led to our abundant modernity. They provide a detailed history of human development, from the African rainforest through the “Great Enrichment” of the last two centuries, and document the factors that led us from the former to the latter. Though there are plenty of lessons in this section, one noticeable theme is humans’ unique ability to escape their primitive, selfish, and myopic “zero-sum” existence and instead engage in the free, cooperative exchange of both stuff (trade) and knowledge (innovation) for their long-term, mutual benefit.

A few examples regarding trade:

-

“Over time, …people have developed sophisticated forms of cooperation that increase their wealth and chances of survival. Consider, for example, trade and exchange. In his 1776 magnum opus The Wealth of Nations, the Scottish economist Adam Smith (1723-1790) wrote about humanity’s “propensity to truck, barter, and exchange one thing for another.’ Smith noted that trade is one of the characteristics that distinguishes humanity from non-human animals…..”

-

“The adoption of silver as currency meant that for the first time in history there was a universal means of exchange. That removed the need to barter in long-distance trade, making trade much easier and more profitable. These economic changes meant that as the population recovered from famines, plagues, and wars, long-distance trade returned and even exceeded its previous peak in the 13th century. Urban trade hubs rebounded, and more types of goods were traded, allowing for greater specialization among regions.”

-

“Far-reaching developments, such as the liberalization of trade, allowed the benefits of industrialization to spread globally. Trade volumes rose, costs fell, and, as reflected in the process of price convergence, markets became global. The gold standard and the invention of the telegraph made capital transfers easier. Attracted by higher profits, investment flowed from more developed to less developed countries. The Industrial Revolution marked a definite break with our Malthusian past.”

And innovation:

-

“What’s truly beautiful about humanity is that our social and technical innovations complement each other. Less social people might invent more often, but they need a predominantly social population in order for their inventions to proliferate and benefit humanity as a whole. Furthermore, as we saw with toolmaking, stones, and fire, society multiplies the positive effects of technical innovation. The internet is a great modern example of that social dynamic.”

-

“Technology makes our lives easier, but the success of our species is contingent on our ability to cooperate and organize as a society.”

-

“In The Rational Optimist, [Matt] Ridley explains the process of innovation in terms of sex. Imagine how slow evolution would be if animals were to reproduce asexually. There would be random mutations in each generation, but the vast majority of those mutations would be useless. Sex brings the genes of two separate individuals together, drastically increasing the possibility that two previously useless mutations will have a positive effect when combined. Ideas obey the same principles. More people can generate more ideas. Even if only a small fraction of humans can generate a good idea, the number of good ideas will grow in proportion to population growth.”

And a bit of both:

-

“So, innovation relies on population growth and the freedom to exchange goods and ideas. The larger the population, the larger the market. The larger the market, the more specialized a population can become. The more specialized a population becomes, the more prosperous it grows. Furthermore, a higher degree of specialization makes innovation more likely and technological regression less likely.”

-

“Inventions begin with ideas that emerge from the human mind…. Oral and written language allows human beings to communicate complex ideas with one another across space and time, allowing knowledge to grow and be shared. Individuals then demonstrate their ideas with inventions. Finally, people test their inventions in the marketplace. An innovation, therefore, is a market-successful (or, to use Deirdre McCloskey’s term, ‘trade-tested’) invention.”

-

“Mercifully, countries that lack intellectual capital to spur innovation and growth can access ‘ideas that are available in the rest of the world… partly through unimpeded flows of the capital goods that are produced in the industrialized nations of the world. These goods embody many new ideas.’ Dissemination of intellectual capital, then, also depends on ideas. Specifically, it depends on abandoning the discredited idea of economic self-reliance… as well as embracing free trade. That’s to say that innovation and economic development depend on an intellectual shift from a mindset that sees foreign investment and the operation of multinational corporations (MNCs) as tools of capitalist exploitation, to a mindset that sees foreign investment and MNCs as sources of valuable and growth-enhancing knowledge.”

I could go on, but I think (hope) you get the idea.

Citing economic heavyweights like McCloskey, Douglass North, and Paul Romer, P&T document the factors that changed a few centuries ago and allowed humans to generate superabundance: cultures (of tolerance, knowledge, commerce, innovation, and trust); institutions (including democratic governments); markets (to test and spread things and ideas); infrastructure (even mundane things like modern accounting); and people (the more, the better). And, of course, human intelligence is critical. But superabundance’s secret sauce, it seems to me (at least), is humans’ pursuit of mutually beneficial exchange. All the other things merely facilitate or support those exchanges: They’re the bowl and whisk you need to make the sauce, not the sauce itself.

So What Threatens It?

If that’s all too much optimism for you, P&T end with a warning about three things that threaten a future of continued human innovation and Superabundance:

Since ideas are not made of matter, the laws of thermodynamics do not apply. Innovations can thus create exponential new value. But will we continue to innovate? The authors can see three potential threats on the horizon. The first is an environmental-panic-induced decline of the global population. The second is a potentially serious decline in the freedom of expression. The third is the omnipresent danger of further restrictions of the freedom of the market.

Each of these threats is in some way an “enemy of exchange” (my term). Speech restrictions and self-censorship curtail the exchange of ideas (especially controversial—but potentially innovative—ones). Onerous taxes and regulations curtail the domestic and cross-border exchange of goods, services, and knowledge. Eco-catastrophism and depopulation curtail the vehicles of exchange (i.e., markets and people).

I remain optimistic that superabundance can continue, despite these threats. In the book we see, for example, long-term declines in the time prices of even heavily regulated things like sugar or pickup trucks (which both face high trade barriers), and ehousing (which faces trade, land-use, and other restrictions). As we dorks commonly joke on Twitter and elsewhere about that old Jurassic Park line, the market … uhh … finds a way.

Nevertheless, the threats to superabundance remain quite real and are certainly more prevalent (or, at least, more vocal) today than they were even a decade ago. Prominent lawmakers and pundits openly lament American “consumerism” and pervasive “market failures”; they cheer higher prices, preach eco-doomerism, decry cross-border investment and innovation, and see shadowy foreign, corporate, or environmental bogeymen around every corner. On these and other grounds, they eagerly work to restrict humans’ relatively free exchange of goods, services, and knowledge, seemingly oblivious to those transactions’ immense value, far beyond simply “cheap stuff.”

Superabundance can hopefully serve as an incredible reminder and warning—to them and us all.

Chart of the Week

Please note that we at The Dispatch hold ourselves, our work, and our commenters to a higher standard than other places on the internet. We welcome comments that foster genuine debate or discussion—including comments critical of us or our work—but responses that include ad hominem attacks on fellow Dispatch members or are intended to stoke fear and anger may be moderated.

With your membership, you only have the ability to comment on The Morning Dispatch articles. Consider upgrading to join the conversation everywhere.