Dear Capitolisters,

Last week, House Democratic leadership introduced a gargantuan piece of legislation purportedly intended to bolster American “competitiveness” and counter China’s rise. The bill itself is way too big to summarize and analyze in this space, but it nevertheless provides us with a teachable moment about how not to legislate economic policy in the United States and, quite frankly, about much of what’s wrong with congressional policymaking in general these days.

COMPETES? Really?

Indeed, the America COMPETES Act of 2022 is a classic example of how Move Fast and Break Things—a book highly critical of “libertarian” Big Tech bros’ disruption of the American economy—today more aptly applies to congressional economic policymaking. The bill itself is 2,912 pages long; the section-by-section summary is a mere 109 pages (12 sections in all); and the “factsheet”—a term that has apparently lost all meaning—clocks in at a paltry 20. The bill was unveiled— “introduced” is imprecise, as the House Rules Committee simply grafted new text onto a previous bill—last Tuesday and will be considered starting this Wednesday. I’d be willing to bet that, as of that date, there probably isn’t a single person—and certainly not more than a baker’s dozen—with a firm grasp on the entire thing, even at a high level. From what I’ve read, the bill is a mix of a few good things and a bunch of awful ones. On the good side, for example, the bill—

-

Exempts STEM Ph.D.s from green card numerical limits;

-

Establishes a startup visa program for immigrant entrepreneurs;

-

Provides refugee status for residents of Hong Kong and Xinjiang, as well as special visas for highly skilled Hong Kongers;

-

Modestly extends (for two years) the Generalized System of Preferences program, which exempts certain imports from developing countries (not China) from U.S. tariffs; and

-

Reaffirms the United States’ commitment to the World Trade Organization.

Each of these could be improved (see, for example, this point on STEM immigrants), but they’re generally in the right direction—leaning into the openness and dynamism that makes America great—and enjoy support across the political spectrum.

On the other hand, those good provisions are drowned out by a whole host of bad ones (“The House stuffed the bill full of Democratic priorities,” says Politico), including:

-

A $52 billion slush fund for semiconductor manufacturers who don’t need the money and are already investing here (see my deep dive here; or this new one from Reason’s Eric Boehm).

-

A $45 billion buffet of grants, loans, and loan guarantees to address “supply chain resiliency” issues—subsidies that one U.S. manufacturing group literally celebrated as a “pot of money” it’s eager to dip into. (To give you an idea of just how laser-focused this initiative is: The new Department of Commerce “Supply Chain Resiliency and Crisis Response Office” will be tasked with “supporting the creation of jobs with competitive wages, including by preserving existing collective bargaining agreements and supporting union organizing efforts.”)

-

Specific subsidies for solar panel manufacturers ($3 billion), electrical grid equipment manufacturers ($375 million), drug manufacturers ($100 million), other medical goods manufacturers ($1.5 billion), makers of Open Radio Access Network equipment ($1.5 billion—never mind O-RAN’s problems), as well as new “Buy American Seafood” grants (of course) to promote the consumption of “domestic marine fishery products” and new Buy American mandates for aerial drones.

-

Billions more for top-down “strategic” R&D initiatives, including through 10 different “Regional Technology and Innovation Hubs.” (Read Mercatus’ Adam Thierer on why this approach to American innovation is so wrong-headed.)

-

An amendment to remove public notice and due process checks on the Treasury Department’s enforcement abilities under the Bank Secrecy Act, potentially crippling the cryptocurrency industry in the process.

-

A provision that addresses the online sale of dangerous or harmful counterfeit goods but is also “a clumsy cudgel that is costly, harmful to consumers and small businesses, and raises real concerns about privacy” and “ may do significant harm to smaller online sellers and marketplaces.”

-

A major expansion of the failed Trade Adjustment Assistance program (which gives workers allegedly displaced by import competition extra unemployment and other benefits)—even as TAA use has declined in recent years (while imports have increased!).

-

Yet another amendment to our already protectionist U.S. trade remedy (anti-dumping, countervailing duty) laws—which we discussed just last week—that would make it even easier (and faster) for certain domestic manufacturers and unions to get the government to apply these special duties on imports from any country, not just China.

-

The elimination of various exemptions from U.S. tariffs—for example on low value (“de minimis”) transactions from China and Vietnam, or for finished goods under the “Miscellaneous Tariff Bill.”

-

A sweeping new system for government regulation of outbound investments—again, not just to China—by U.S. firms on undefined economic (“offshoring”) or security grounds.

I could devote a blog post, if not more, to each of these items—and I’m quite confident I’m missing others. But the last item, the outbound investment system—U.S.-based companies investing in foreign countries—warrants special mention. As law firm Covington helpfully explains, the bill would make the United States “the first major Western advanced economy to adopt a broad-gauged outbound investment screening process” but is so “sweeping in scope and lacking in specifics” on covered transactions, implementation, and procedures that it could conceivably cover basically any industry and any investment in any country. A new Rhodium Group brief adds that this kind of system would have serious implications far beyond the U.S.-China relationship, not only breaking from the U.S. foreign policy tradition of championing “a free, open global investment environment” but also prompting other governments—including many U.S. allies—to consider similar regimes and potentially hurting American companies’ competitiveness:

Openness and a lack of red tape for global investors has helped make the US the dominant country in global cross border capital flows. At the end of 2020, according to the OECD, the US had the world’s largest stock of both inward and outward FDI, with $10.8 trillion and $8.2 trillion, respectively.

A US outbound screening regime would not only affect the assets and competitiveness of US companies in the Chinese market but could also impact the US operations of foreign companies. Many globally operating MNCs have operations in the US, either for specific purposes like R&D or as a hub to serve the Americas. According to the [proposed legislation], foreign-owned subsidiaries in the US would be subject to outbound investment controls as well (foreign companies thinking about shifting production activities involving national critical capabilities to countries of concern would need to report the transaction to the committee, and could face mitigating action).

At a minimum, this increases the cost of doing business for US-domiciled companies, complicating cross-border operations relative to other countries. Under certain circumstances we could see both American and foreign companies shifting IP-intensive operations or assets out of US jurisdiction to avoid being covered under the new regime.

Covington rightly adds that U.S. companies routinely invest abroad and then bring a significant portion of those revenues back home, spending on higher value-added or more capital-intensive activities like R&D, marketing and design, or advanced manufacturing. U.S. multinationals also invest abroad to service those markets—not to sell back to the United States. It’s thus no surprise, then, that the data show that U.S. expansion abroad usually supports expansion—and jobs—back here too.

These and many other issues raised in the bill warrant serious debate and consideration—especially given the equally serious national security concerns that might support some restrictions on trade and investment (at least in theory). But, sure, let’s ram this sucker through in a week.

Bigger Problems

Now, I am assured by the plugged-in folks at Politico that the House will consider amendments to the COMPETES Act this week, and that whatever final form the bill takes will be changed again during the House’s conference committee with the Senate, which passed its own “competitiveness” bill—the similarly-porky U.S. Innovation and Competition Act (USICA)—last year. Some of the bad stuff—and unfortunately some of the good—above will surely change again or be removed entirely in the coming days and weeks.

But that assurance, really, misses the bigger problems with this kind of process—one that simply packages a bunch of unrelated individual committee priorities into a massive “omnibus” bill, rushes to pass that just-released behemoth with little or no scrutiny, and then melds it behind closed doors with the other chamber’s version so that the final Frankenstein bill can be voted on in an equally rushed and blind manner.

For starters, there’s the politicization and “log-rolling” that always accompanies these types of bills. Recall, for example, that the initial vehicle for the sprawling, clumsy America COMPETES Act and USICA was an “Endless Frontier Act” proposal that would have juiced government spending on basic research (which is now an afterthought) by $100 billion over a decade. Indeed, Politico just yesterday acknowledged—in a classic case of saying the quiet parts out loud—that the current “China competitiveness” bill is really just a vehicle for ramming through those semiconductor subsidies and thereby giving Biden a big political win before his State of the Union address. That semiconductor subsidy package, moreover, was originally a mere $10 billion, grew to $27 billion under Biden, then rose to $50 billion, and seems to have now topped out at its current $52 billion (after Michigan lawmakers threw in the last $2 billion for chips that Detroit automakers want). Various analysts now estimate that the overall House package spends about $320 billion (with little, if any, offsetting revenue).

Among all this extra wheat will surely be hidden chaff that sneaks past the finish line and then embeds itself in U.S. economic policy for years to come. A new Reason Foundation report provides a good historical example of just this very thing: The multibillion dollar Rebuilding American Infrastructure with Sustainability and Equity (RAISE) grant program—first started in the 2009 stimulus bill, designed to sunset years ago, and intended for national transportation projects—has been repeatedly reauthorized even though only a handful of projects can be properly considered within the original program’s scope. Politics, unsurprisingly, appears to be the program’s big motivator: “41 of the 90 projects funded went to districts or states represented by lawmakers on Congress’ various transportation and finance committees” and “White House has near-total discretion to award these grants as it sees fit.” Numerous other examples abound. As we’ve discussed, for example, U.S. trade remedies law is replete with protectionist amendments that snuck through the legislative process on the coattails of “must-pass” bills.

The RAISE debacle also highlights another problem with these massive bills: the high likelihood of implementing an incoherent law that actually undermines itself. Thierer hits on two such examples of this in his piece on the America COMPETES Act. First, the bill seeks to create national champions in all sorts of “strategic” fields, while also expanding federal antitrust power: “Apparently, once America’s grandiose industrial policies magically create global powerhouses in every sector, we’ll need expanding antitrust action to tear them all down and start all over again!” Sigh.

Second, these bills’ inevitable ambiguity—driven by the slapdash drafting and amendment process or something more intentional (and nefarious)—allows for all sorts of unknown (but unsurprising) bureaucratic interpretation and, eventually, conflict:

All the ambiguities associated with a monster measure like this means that agency bureaucrats will be left to fill in all the details for many years to come. It is folly of the highest order to believe that all these agencies will work together in a tightly coordinated and consistent way to advance industrial policy efforts or address “strategic objectives.” Anyone currently following the fight between the FAA and FCC over the rollout of 5G wireless networks will know what I am talking about. Moreover, delegating broad authority and big money to all these agencies just further reinforces the rent-seeking instincts of special interests, who will rush to their respective regulatory masters with hat in hand. The presents agencies with an added policy lever to blackmail companies into doing what they want without any new regulations even being issued.

As we relearned during the Trump administration, policy uncertainty can impose real and tangible harms on business output, investment, and employment. Meanwhile, U.S. history is littered—as we’ve discussed in the case of both infrastructure spending and industrial policy—with well-intentioned economic planning initiatives being thwarted by other policies pushing in the exact opposite way (sometimes in the very same law!). In the America COMPETES Act’s case, for example, there’s a real chance that the outbound investment screening process would harm American companies’ global competitiveness and push important R&D offshore. It also makes zero sense to subsidize semiconductor, solar panel, and other manufacturing while simultaneously boosting laws—trade remedies, especially—that would allow for the imposition of new tariffs (taxes) on the industrial inputs that those same manufacturers need. (Trade remedies most often target—quite illogically—industrial inputs like metals and chemicals.)

If Congress really intends to strengthen U.S.-based companies in our battle against China for global economic supremacy (or whatever), they sure have an odd way of showing it.

A Better Way Forward

I don’t expect for a second that members of Congress will wake up tomorrow and become free market libertarians hell-bent on implementing my personal economic agenda, but there are plenty of policies buried in the America COMPETES Act and USICA that are—unlike the current dog’s breakfast of political payouts—directly relevant to China, American economic competitiveness, and the Endless Frontier Act’s original goal of boosting federal funding for basic research in the United States. This includes, for example, the COMPETES Act’s immigration provisions; the USICA’s trade liberalizing provisions (which were removed or watered down in COMPETES); basic research funding that is untied to chosen regions, workers, industries (see Thierer here for more); and some of the COMPETES Act’s general education and training funding (for things like apprenticeships and STEM education). I’m sure there’d be things in that kind of targeted, coherent package—one considered under normal legislative order and subject to intense public scrutiny—that I didn’t like, but it’d be light years closer achieving Congress’ competitiveness objectives than the slapdash monster we may very well get—a package that not only adds another, expensive layer of industrial planning, bureaucracy and protectionism atop the many layers we already have, but could actually undermine our nation’s still-strong industrial and scientific might while boosting China in the process. (Reforming those other layers—new example here—would of course be good too, but let’s not get greedy here.)

In the alternative, maybe the sequel to Move Fast and Break Things could take a look at Congress.

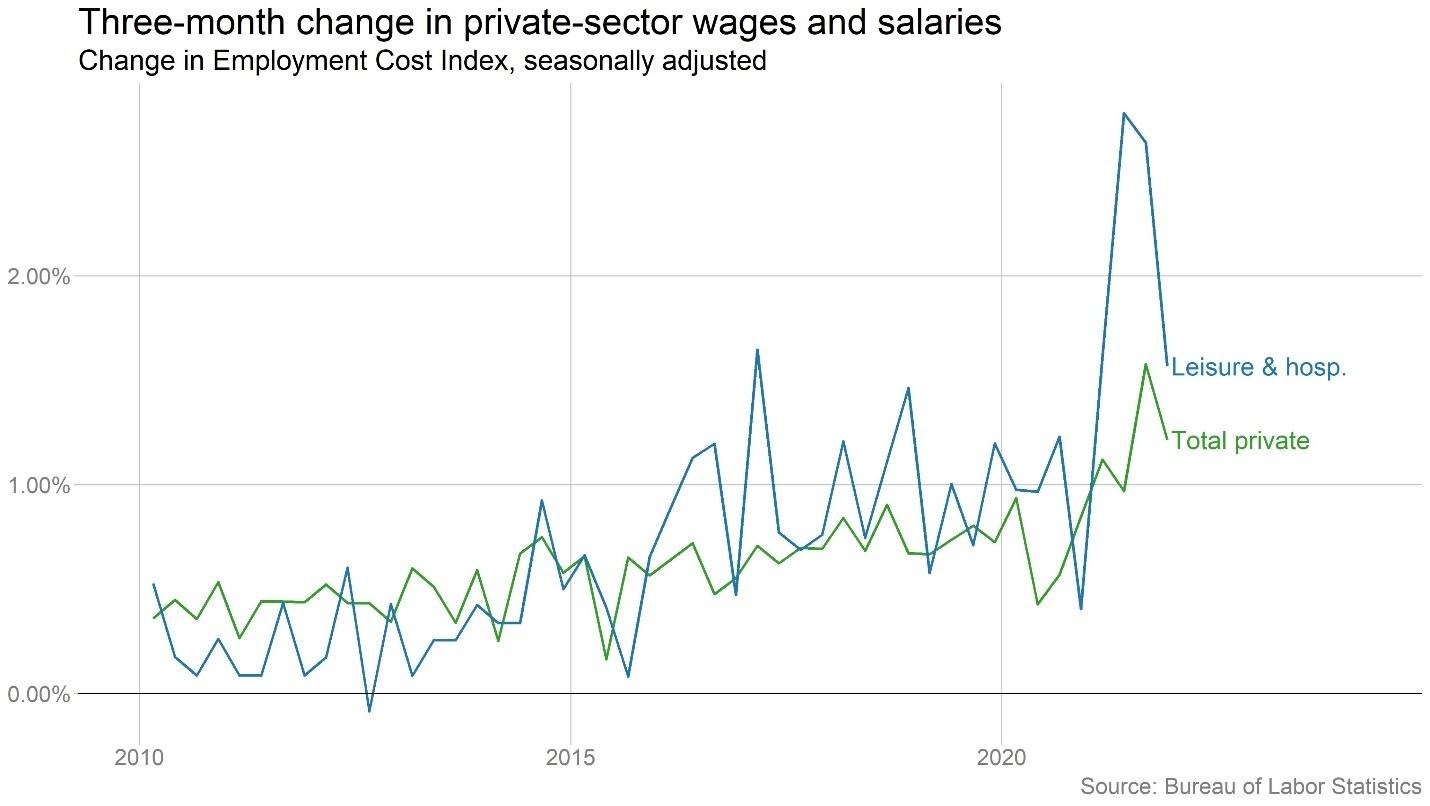

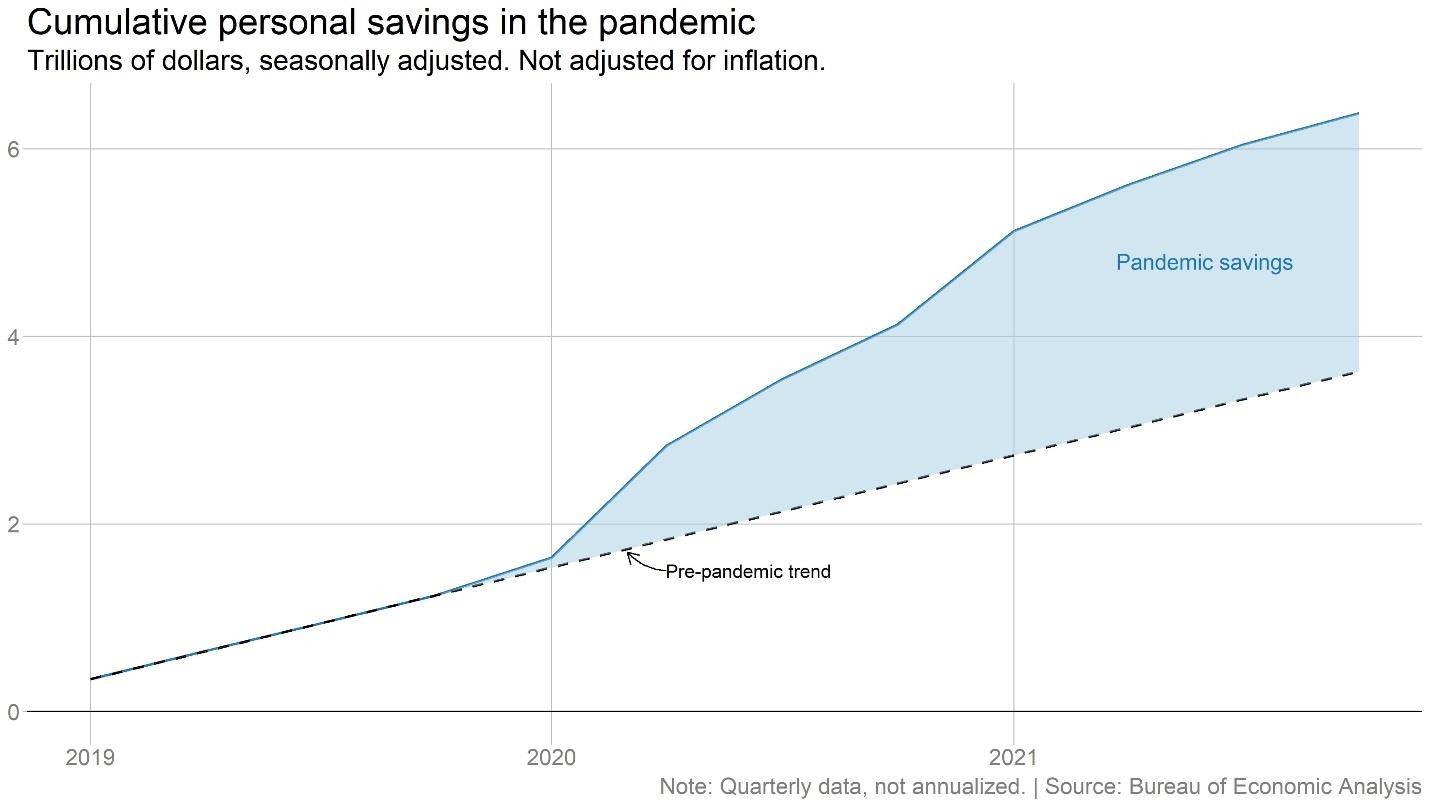

Chart(s) of the Week

Please note that we at The Dispatch hold ourselves, our work, and our commenters to a higher standard than other places on the internet. We welcome comments that foster genuine debate or discussion—including comments critical of us or our work—but responses that include ad hominem attacks on fellow Dispatch members or are intended to stoke fear and anger may be moderated.

With your membership, you only have the ability to comment on The Morning Dispatch articles. Consider upgrading to join the conversation everywhere.