Dear Capitolisters,

When pressed to suggest a country that the United States should emulate, industrial policy fans often point to South Korea. It has a relatively large and advanced manufacturing sector (in terms of both output and employment), a persistent trade surplus, and a government that hasn’t been shy about thumbing the economic scale to support favored industries. Thus, so the theory goes, the Korean government has been successful in using industrial policy not only to generate more “good jobs” and “strategic industries” than the United States, but also to be less “dependent” on foreigners for essential goods in times of crisis (war, pandemic, etc.). So, obviously, we can and should do the same.

Leaving aside the obvious perils of cross-country comparisons (nations and governments are very different), this line of argument contains a nugget of truth—one that I think some industrial policy critics ignore to their detriment: Dig into massive, globally competitive Korean companies like Samsung or Hyundai, and you’ll surely find some of the government’s fingerprints, and Korean policy probably has shifted the economy’s composition toward manufacturing and specific industries.

But that’s not where the “success” story ends, and recent events in Korea and elsewhere have revealed one of the big downsides of explicit government policies designed to tilt a nation’s economic playing field toward “strategic” or “essential” manufacturing industries and exports: It can actually boost a nation’s fragility, rather than reduce it.

South Korea’s Sunny Day Successes

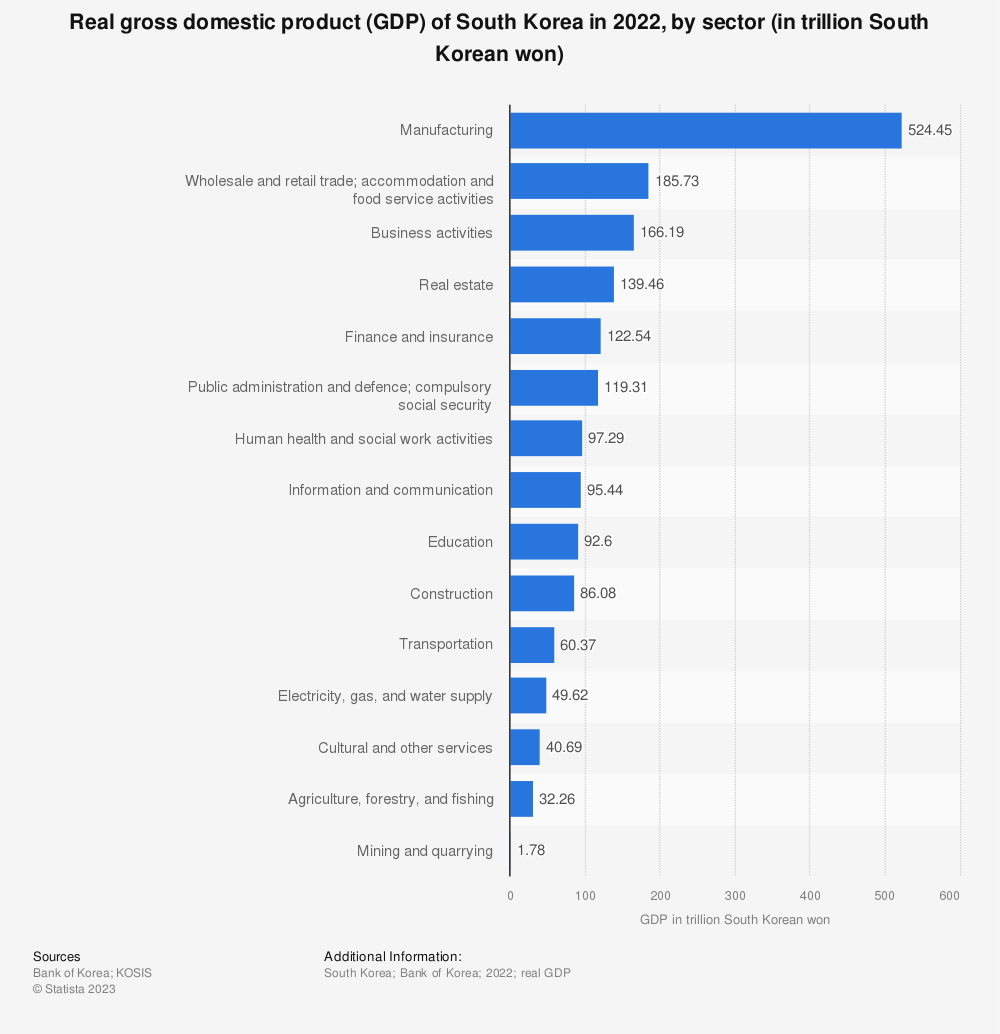

As noted, Korea’s economy—and some government policy—has undoubtedly focused on certain types of manufacturing. Last year, for example, the industrial sector accounted for about 25 percent of Korean gross domestic product, with particular strength in a few key industries, such as automotive, shipbuilding, and electronics (especially semiconductors). By contrast, the United States—while still the world’s second largest manufacturing nation overall—devoted only about 11 percent of its economy to manufacturing in 2021:

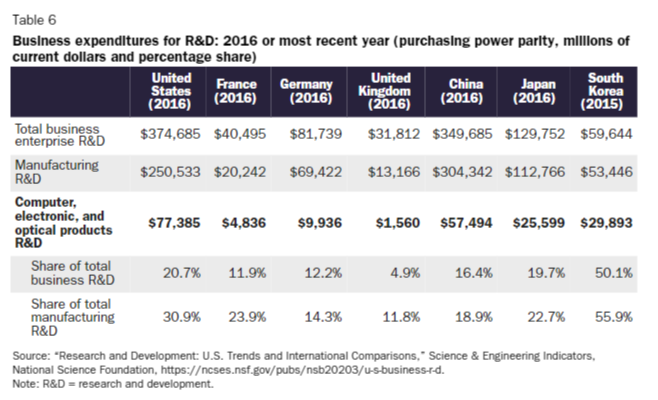

Electronics are a particular area of emphasis in Korea’s manufacturing sector. For example, the nation devoted more than 50 percent of its total R&D spending in 2019 to just electronics manufacturing, which of course includes lots and lots of semiconductors:

Korea has also run persistent trade surpluses since the mid-1990s:

Finally, there’s little doubt that Korean production of these and other “strategic” goods has produced discrete benefits for the country and, via prolific exports, the world. Brands like Samsung, LG, Hyundai/Kia (plus their cousin Hynix for semiconductors), and Daewoo are top players in their particular industries. Koreans directly employed by or selling to these companies surely benefit from their existence.

Put it all together, and you have an industrial policy dream—at least in the good times.

When the Good Times End

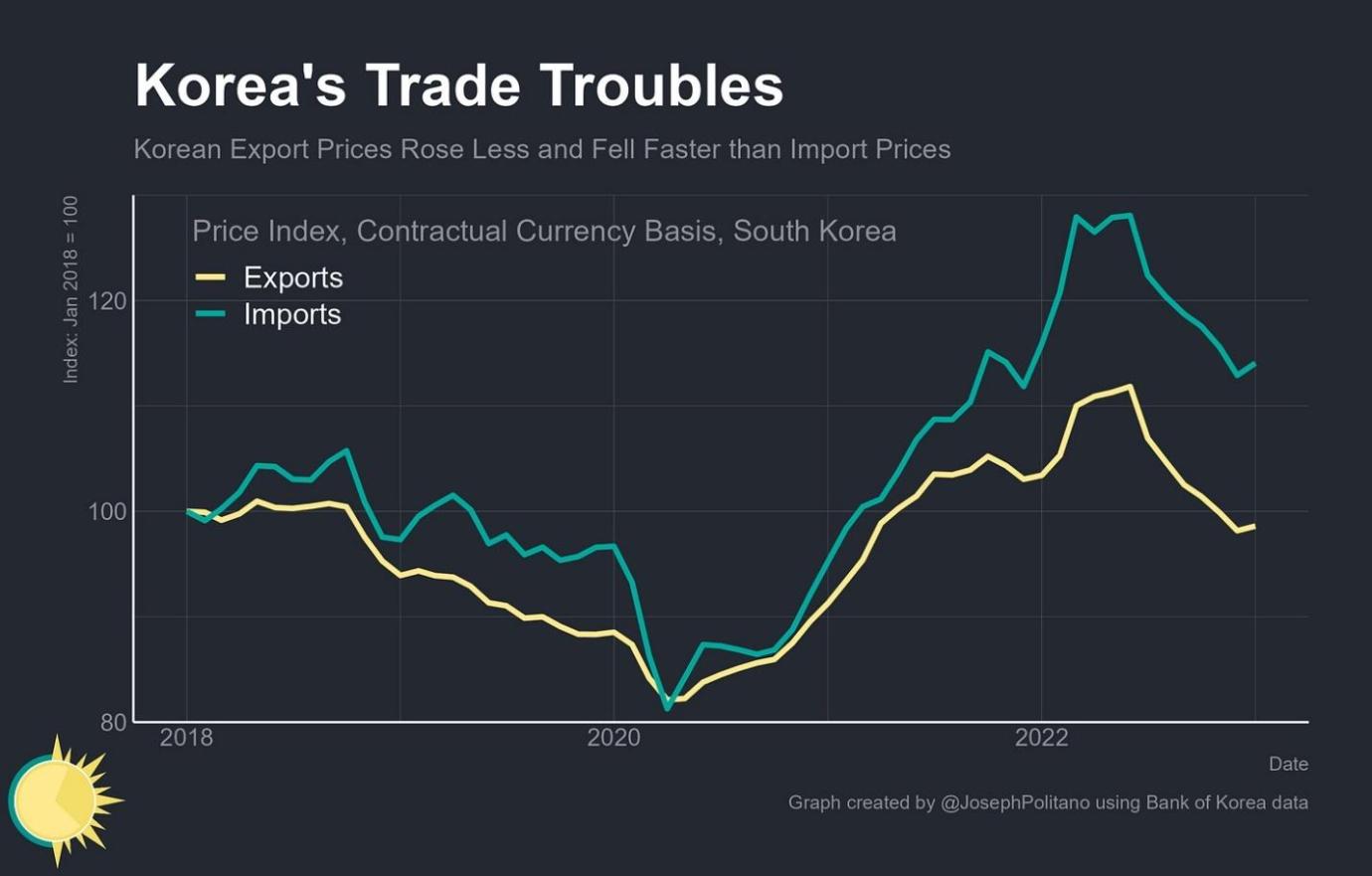

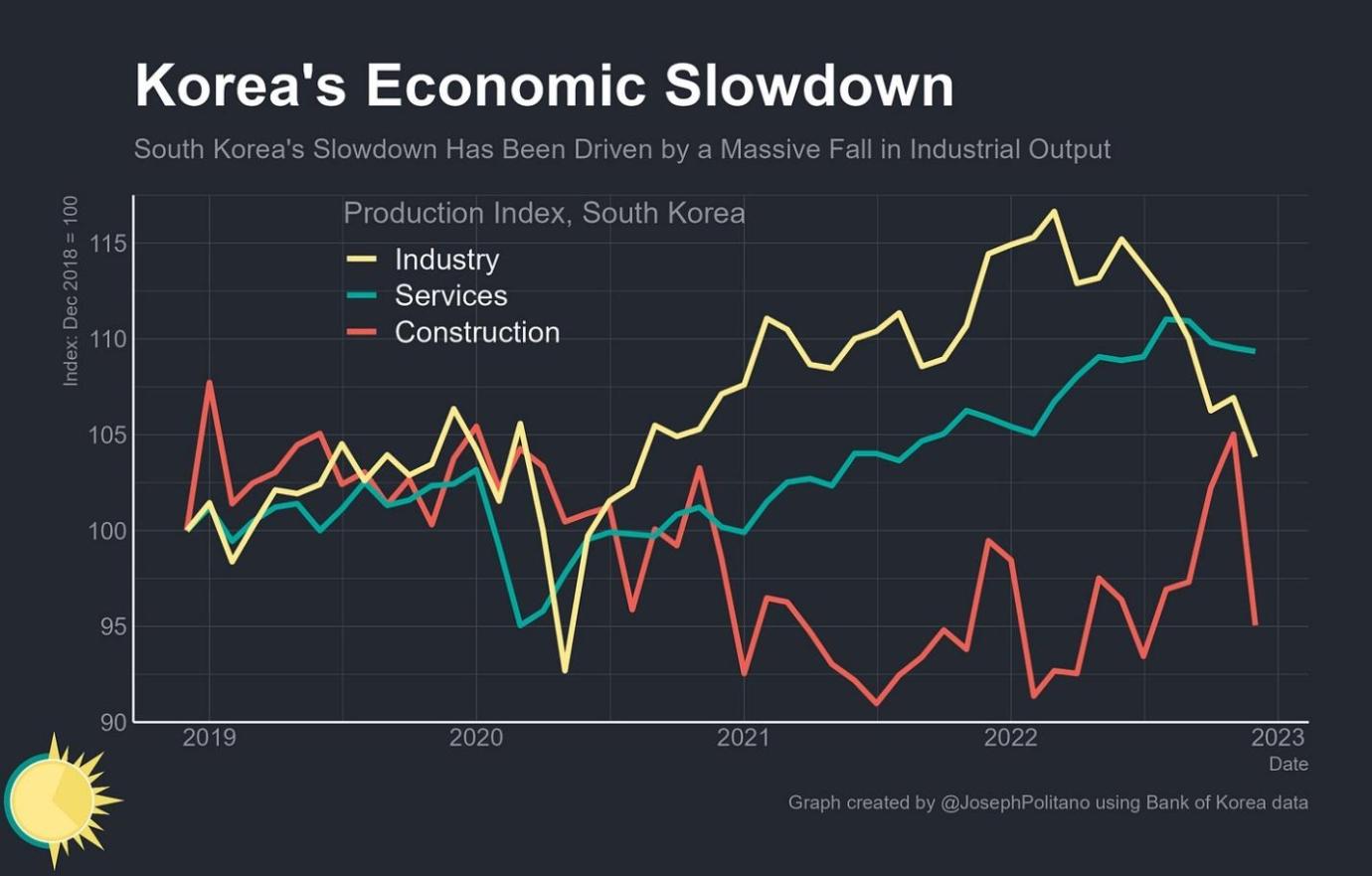

The good times, however, don’t last forever, and recent events reveal a big economic downside to this kind of industrial strategy. In particular, global demand for the stuff Korea makes and exports—and thus the stuff on which its intentionally lopsided economy depends—has declined significantly, thanks to a combination of central bank tightening, Chinese economic turmoil, and consumers’ post-COVID shift back to services after almost two years of gorging on goods. As a result, economist Joey Politano recently showed, Korea’s economy is in bad shape today:

The kind of large, high-tech manufacturing goods that the nation excels at exporting—cars, computers, semiconductors, cargo ships, consumer electronics, and the like—have seen demand wane from their COVID-era highs amidst a global economic slowdown and the rebalancing of consumer demand toward service consumption. Meanwhile, prices for the food and energy that the nation must import have surged to new highs—all the while China, its largest trading partner, deals with the aftershocks of COVID, and Korean property prices continue falling amidst higher interest rates. Finance Minister Choo Kyung-ho warned the country will face “a complex crisis for a considerable period” as he pledged support for the nation’s struggling industries. Meanwhile, GDP contracted by 0.4% in the last quarter of 2022.

Politano then shows how Korea’s exports declined dramatically in recent months:

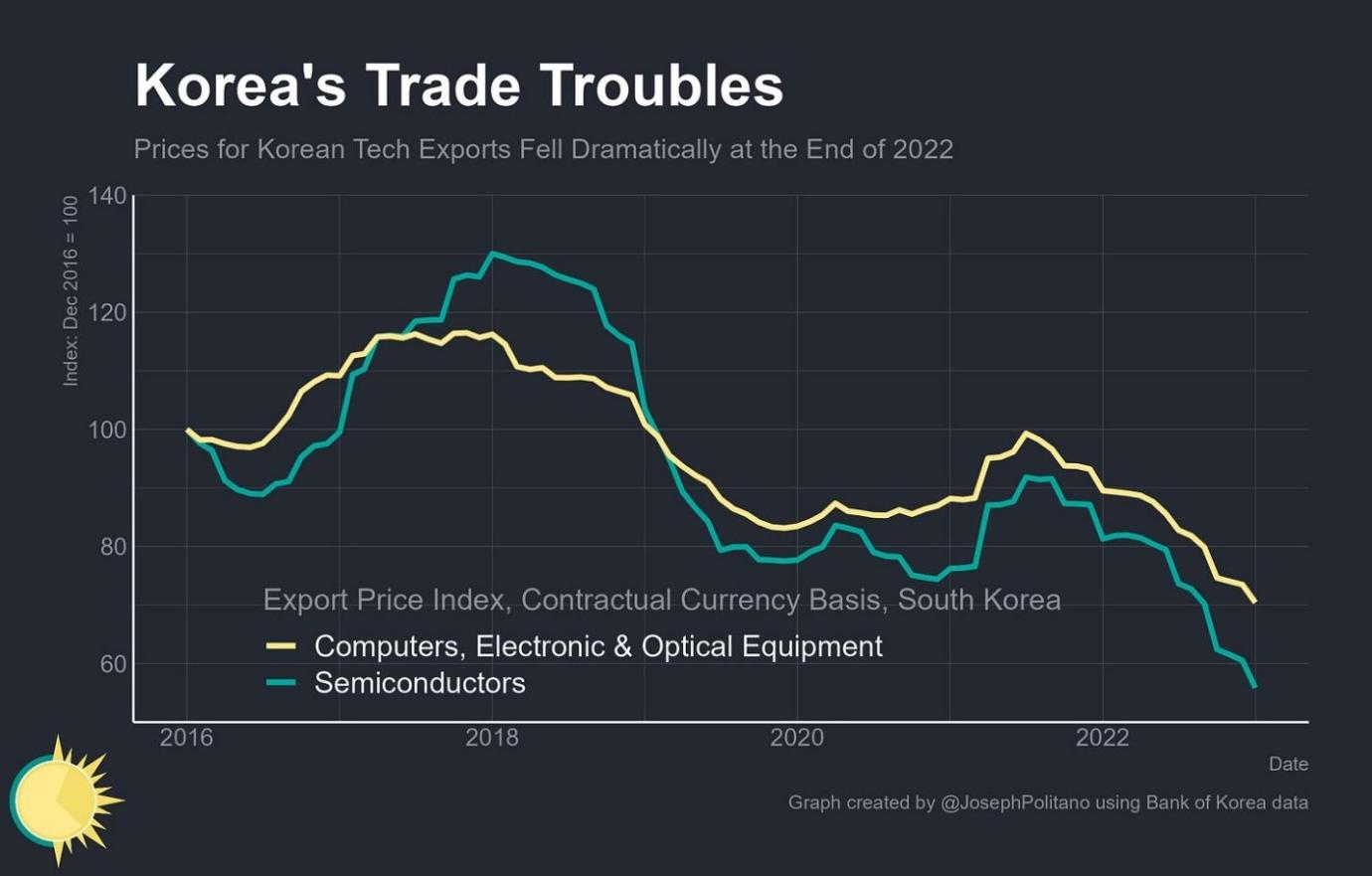

He adds that exports of electronics and semiconductors were especially hard hit:

And this weakness, in turn, caused a “massive” drop in Korea’s industrial output …

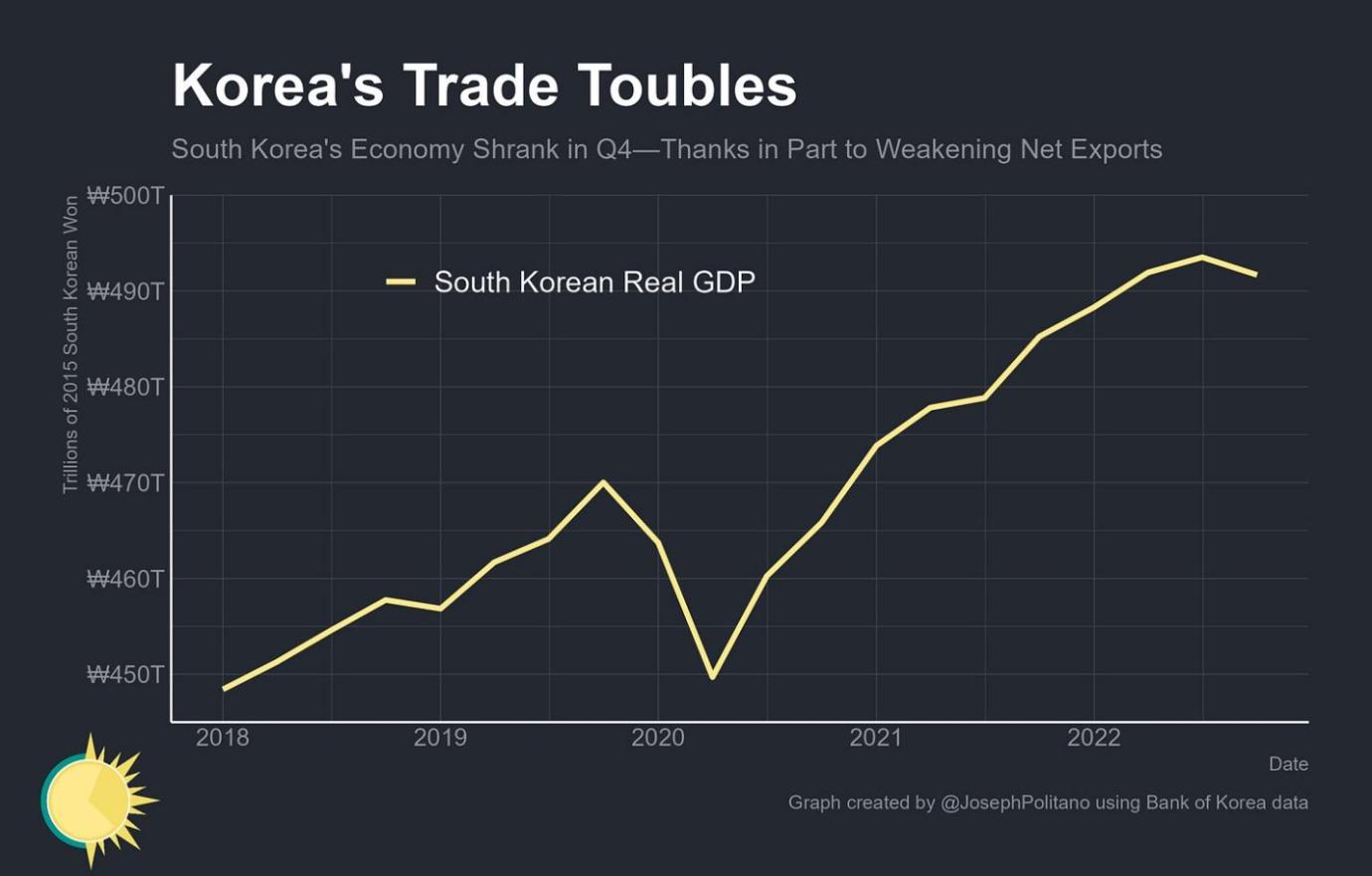

… and thus its GDP:

Not all of these troubles can be laid at the feet of Korean industrial policy, but to the extent it actually was “successful” in shaping Korea’s economy and boosting certain companies above others—it now deserves some of the blame for today’s problems. As Politano notes, Korea’s economic contraction and future troubles are owed to the fact that it is “overexposed to the manufacturing and fixed investment slowdowns that are now hitting most high-income nations.” This “overexposure” is particularly an issue for a country like Korea, with so much export-driven growth: “the downside to Korea’s economic model is that they remain much more dependent on global market forces than most high-income nations—hence the speed of the recent fall in economic output.”

So much for that mercantilist “resiliency,” eh?

Lessons Abound

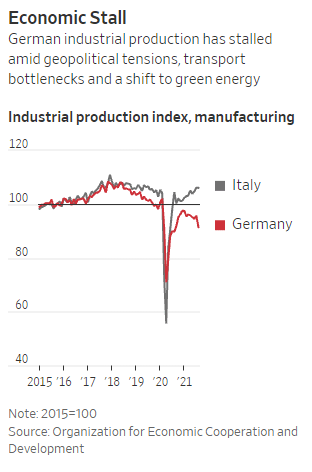

Korea, it should be noted, isn’t alone in this regard. As you may recall, similar troubles arose in Germany—another industrial policy darling—even before the Russian invasion of Ukraine sent all of Europe into a tailspin:

As the Wall Street Journal reported a couple years ago, moreover, Germany’s economic struggles weren’t just a COVID-19 problem, either (emphasis mine): “German industrial output and exports began stagnating in 2017, posing a problem for an economy where some 30% of jobs and output are tied to overseas demand, roughly four times the share in the U.S.”

Both cases provide some broader lessons about using government policy to tilt the economic scales toward preferred sectors or industries:

First, using industrial policy to pick “strategic” winners and losers isn’t just a problem when the government picks the wrong sector, industry, or product (though that certainly is a problem). It can also bite when the government actually picks a winner, for example by creating an economy that’s too economically (and politically) reliant on the winning companies and ends up losing even bigger when, for whatever reason, the national champions face tough times. In Korea’s case, it may have seemed smart in, say, 2019 to funnel so many finite resources toward electronics, but that “success” also sowed the seeds for future problems when global demand for those products collapsed and an entirely different set of “unfavored” goods or services was suddenly in high demand. It also raises the question of the policies’ opportunity cost: Would Korea actually have been better off today if all those government-directed resources had been deployed differently and the economy wasn’t so “overexposed”?

In this regard, consider the more diversified—and, up until very recently, less industrial policy-inclined—United States. We might have looked like an economic laggard last decade but sure look better (and more “resilient”) these days, with world-class production of suddenly important goods like vaccines and petroleum products (which, by the way, have been exported to Korea), new innovations like generative artificial intelligence (e.g., ChatGPT), and a still-growing services-based economy. The collapse of one important sector or industry will still hurt (see, e.g., banking today), but—barring some sort of major contagion—probably won’t collapse the economy because lots of other sectors will keep humming along. And as long as overall productive capacity is high (spoiler: it is) and the economy remains open, market actors—consumers, producers, investors, etc.—will adjust to whatever comes our way.

Economic openness and diversification can’t, of course, protect against all economic crises—bad stuff happens and contagion is real—but widespread, long-term calamities are less likely when the state hasn’t been throwing all of its economic eggs in one basket, regardless of how “strategic” that basket might seem at the time.

Lunches, in other words, remain not-free.

Second, and relatedly, economies heavily tilted toward manufacturing and exports—even if that production is more diversified—aren’t actually all that “resilient” at all, because they crucially depend on overseas demand (and thus the economic and foreign policy of other nations) for growth. In theory, these exporting countries can cut off foreign consumers for economic or geopolitical reasons, but the real world has repeatedly shown that this rarely happens and, when it does, alternative suppliers at home or abroad arise quickly to fill any such void. It’s thus consumers, not producers, really calling the shots, as long as their economies remain relatively open and dynamic. The Peterson Institute’s Adam Posen explains this well using an example that we’ve also recently explored here at Capitolism:

In reality, market economies adapt quickly to shortages; dominant suppliers almost never boycott selling to customers. Also true is that shortfalls in supply are much better addressed through trade and, in the case of some technologies, the stockpiling of strategic reserves.

Take the European Union’s response to stoppages in oil and gas supplies after Russia’s invasion of Ukraine. Eurozone economies adapted to higher and more volatile energy prices far more rapidly than most expected. Prices even dropped after European economies stopped demanding so much supply. The same has been true at every juncture when there has been an interruption in supply or when energy exports have been withheld; in 1973, after a Saudi-led oil embargo, Western economies shifted production and consumption patterns within a couple of years.

Yes, a supplier of a critical commodity with malevolent intent can cause pain via temporary shortages, but an effective response is to stockpile strategic reserves and turn to trade with other places.

We’ve seen similar things with cobalt and rare earth minerals (and, it seems, lithium)—when market actors are free to adjust, high prices and shortages are usually temporary. And, as we learned from the United States’ baby formula and COVID rapid test debacles, supply crises can be deepened and prolonged where the U.S. government has maintained high trade barriers and instead tried to subsidize or otherwise plan its way to prosperity. The baby formula crisis, in fact, might still not be over:

*Insert audible sigh here*

Anyway, Posen also importantly notes that, when baddies do impose export restrictions, it’s usually the exporters—not “dependent” importers—who end up suffering the most (emphasis mine):

Meanwhile, Russia did not get anything terribly useful in diplomatic terms when it tried to weaponize Europe’s dependence on its oil and gas. When Russian President Vladimir Putin cut off gas from the Nord Stream 1 pipeline in mid-2022, he induced Germany and other European economies to reduce their dependence on Russia while strengthening Europe’s support for Ukraine. His dominant supply position did not even prevent the EU from encouraging Ukraine to turn its way in recent years. And despite Putin’s threats to cut off global supplies, Russia has up to the present day continued to keep oil and gas exports flowing to other buyers.

In other words: In an actual war situation, with a most malevolent supplier making seemingly credible threats, Europe has not been deterred or even swayed. This shows that market economies’ resilience is much greater, and the ability of suppliers to extract concessions much less, than the scaremongering used to justify extreme U.S. industrial policy would suggest.

Amen.

Summing It All Up

Industrial policy typically catches flak when the government subsidizes failures like Solyndra or Foxconn, but even ostensible successes can make economies more fragile and undermine long-term growth. In the case of Korea (and, pre-Ukraine Germany), decades of support for certain manufacturers may have looked like a brilliant move when foreign demand for their goods was high, but it also carries big risks when consumers’ needs turn elsewhere—risks that a more fluid, more diversified, and less export-dependent economy like the United States probably won’t face. (Though Posen rightly recalls how one darling of past U.S. industrial and export policy—Boeing—has produced similar distortions to those occurring on a wider scale in more state-directed economies.) Studies show, in fact, that Korea’s economy actually performed better in periods that featured less government intervention, and that “additional liberalization would have increased national welfare by as much as 10 percent of GDP.” Given recent events, it’s perhaps now easier to see why that might be the case.

Korea and Germany’s problems also reveal the emptiness of a “resilience” strategy that turns away from economic openness and instead tries to boost domestic manufacturing, generate trade surpluses, and end our supposed “dependence” on overseas suppliers to ensure stronger, more stable economic growth in the future. Such strategies might make for good political soundbites and win votes from worried citizens, but they sow the seeds of their own destruction when the winds change—as they always do.

Just ask Korea.

Chart(s) of the Week

Please note that we at The Dispatch hold ourselves, our work, and our commenters to a higher standard than other places on the internet. We welcome comments that foster genuine debate or discussion—including comments critical of us or our work—but responses that include ad hominem attacks on fellow Dispatch members or are intended to stoke fear and anger may be moderated.

You are currently using a limited time guest pass and do not have access to commenting. Consider subscribing to join the conversation.

With your membership, you only have the ability to comment on The Morning Dispatch articles. Consider upgrading to join the conversation everywhere.